Venture Capital Fund(amentals)

A deep-dive into Structures — Performance Metrics — Home Runs

“Ideas that most people derided as ridiculous have produced the best outcomes. Don’t do the obvious thing.”

<<Fred Wilson>>

Well, venture capital is a unique and difficult asset class. Ridiculous unicorns pop-up like black swans and create millions over millions in returns to venture capital funds—once IPOed or exited. It might seem like a cash printing machine from the outside, but it’s not.

It’s a strange world indeed, lets take a deep-dive into this isolated ecosystem by answering some obvious questions, such as how venture capital funds are structured, how they measure success and why home runs are needed to justify their existence.

The GP/LP Structure

The highly simplified illustration shall give you a birds-eye view on how a GP/LP structure for a venture capital fund may look like. For sure, there are plenty alternatives on how to structure the legal side, due to compliance requirements, governance or tax implications for the General Partner (GP), its Sponsors, as well as the Limited Partner (LP). It is very likely that venture capital funds work with Special Purpose Vehicles (SPV).

To give you just one example: The GP could place a SPV between the fund and the investment (here Co.), in order to pool co-investors (usually LPs in the fund or affiliated parties). Lets take a closer look the relevant parties and important aspects.

The General Partner is usually the initiator of the fund, historically the GP commits an amount of 1% of the total committed capital of the fund. The reasoning behind this might be easily explained by the Agency Theory, which explores the relationship between principals (LPs) and agents (GP) in an enterprise. The GP usually has full control of the management and investment decisions, while the LPs have limited visibility or influence on the day-to-day operations.

Therefore, it is expected that the GP has “skin in the game” to align interest. In my opinion the GP commitment (cash contribution, not a management fee offset, or a loan from the fund) has to come out of the managing partners pocket, in order to be meaningful. Furthermore, the GP creates a Private Placement Memorandum (PPM, as well called Offering Memorandum) and a Limited Partnership Agreement (LPA) to attract potential LPs.

The Limited Partners in a VC fund are usually Institutional Investors, (U)HNWIs, Family Offices or Fund-of-Fund Investors. When a LP buys into a VC fund, he commits to a certain investment amount, which can be drawn-down by the GP (usually 15–25% p.a. of the total committed capital, capped at 35% p.a.). The GP is not obligated to call the full amount, the remainder is called unfunded commitment.

The 2/20 Fee Structure, what’s that all about? Well, the “2” stands for 2% management fee (depending on the size of the fund, this number may range between 1.5% to 2.5%) the fee is paid annually, calculated as a percentage of the total committed capital. The “20” stands for 20% carried interest, which is a share of the profits generated by the fund’s investments (here again, this number may be range between 15% to 30%).

To put it in a nutshell, the GP and its Managing Partner manage the LPs money, in order to generate a substantial return, whereby the management fees shall pay the operations and the carried interest is the main incentive.

You might want to keep two relevant aspects in mind :

I. 95% of all venture capital funds aren’t actually returning enough money to justify the risk, fees and illiquidity — benchmark is the “Privat Market Equivalent” (PME).

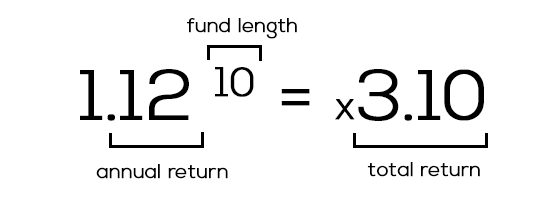

II. A venture capital fund needs to return 3x (venture rate of return) to be considered a good investment. In order to do so, they will have to return 12% p.a. — see the quick math below:

Performance Metrics

Measuring the performance of a venture capital fund is surprisingly tricky, due to the fact that venture capital is a fairly unique asset class. Assets are not priced on an open market, therefore it is difficult to value a venture capital portfolio — there is no real consensus on how to value assets.

Financial terminology might seem confusing, though most of it is pretty straight forward, once broken down. In general, there are two common figures you will come across in venture capital performance.

The Return on Investment (ROI) has two distinct parts “realized returns”, also called “cash on cash (or stocks) returns” or “Distributed to paid-in multiple (DPI)”, which is the ratio of invested capital that has been paid back to LPs in the fund. Secondly, the “unrealized returns”, which reflect the current value of the fund’s position in portfolio companies, which have not been exited yet. The ROI would be the sum of both divided by the initial fund commitment, also “Total value to paid-in multiple (TVPI)”.

The Internal rate of Return (IRR) reflects the annualized effective compounded return rate, which may be earned on the invested capital. It’s a tricky number to report on, as it is difficult to predict the actual size and date of the payout.

To be fair, it’s possible that a venture capital fund ranks in the top tier by IRR, but lags far behind its peers in terms of realized returns. As this wouldn’t be enough of a challenge, valuing the funds portfolio is adding even more complexity. The common methods are:

Last Round Valuation, latest market valuation of the portfolio company multiplied by the funds stake in the company, after dilution.

Comparables/Peer Groups, comparing the earnings of the portfolio company to the price-earning ratio of its peers.

Option Pricing, treating the portfolio companies equity like a set of call options, see Black-Scholes Model.

Venture Capital Method, a complex approach of estimating the exit stake value of the portfolio company, deriving the equity value as a function of risk and time to exit.

Scorecard Method, comparing the portfolio company to recently funded peers, based on the median valuation, adding different parameters.

Net Present Value, the discounted value of the portfolio companies future earnings, while deducting the capital outflows.

There is no gold standard in the industry! Results may vary dramatically — leading to a high degree of uncertainty and variance. The most compelling and nailing conclusion is “Schrödinger’s Valuation Problem” (Credit goes to Mattermark):

“…there are a lot of ways to determine the valuation of a company, and, by proxy, a venture fund’s portfolio. But there is a really important distinction to be made between valuation and worth. A company is worth only what someone (like an acquiring company or the general public in the event of an IPO) is ultimately willing to pay for its shares. There can be many theoretically, technically, and legally correct valuations for a company. But they all collapse down into one final price at an exit event, when the cat is let out of the bag…”

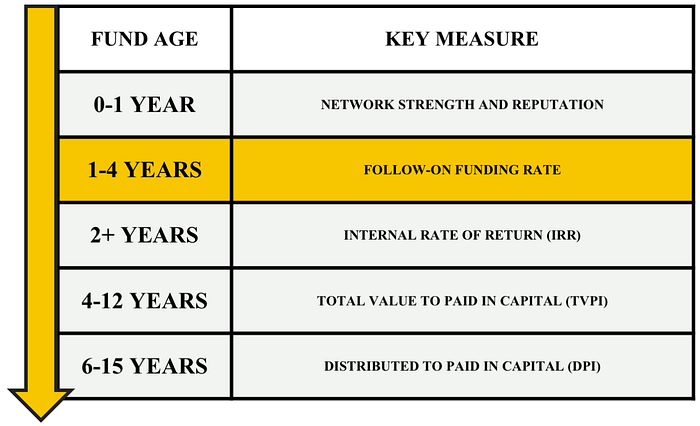

Very pragmatic and true. While researching for this blog post, I came along the chart below, which I think is the most thoughtful approach on how to assess the performance of a venture capital fund “different measures for different times”, especially the importance of the follow-on funding rate:

The Home Run Effect

Maybe a fund does not have to perform like Babe Ruth, but each and every venture capital fund depends on home runs. Bear in mind 5/10 companies will go bankrupt, 4/10 will break-even and 1/10 will do the trick. Though, the 4/10 will still have to be meaningful exits, in order to realize a 3x gross return, which translates into a 2x net return (based on 2/20 fee structure).

I consider a home run as a 1x fund return, which means that one single asset will have to pay back the whole fund, a meaningful exit will still have to return at least 0.3x of the fund (of course, the numbers depend on the actual ownership and the exit size). There is a great article about it by Tomer Dean on TC on “the truth about VCs”.

Overall, there is a lot more to know to be able to assess, whether or not a fund is successful, such as: The vintage year, the size of the fund, first time Vs. second or third time fund (indeed first time funds do perform better in average), the investment strategy, the preferred investment stage, industry and region.

Any thoughts or questions? Reach out! Want read more?

The Angel Performance Playbook

Schrödinger’s Valuation Problem

KPI <kē pərˈfôrməns ˈindiˌkātər> Hunter

Equity, debt and the grey zone in-between.

About myself

I am a passionate and hands-on venture capitalist (+5y), entrepreneur (+7y), mentor and angel investor. After 5 years of flying over 1.000.000 miles, spending 1.200 hours on airplanes, looking at 1.000 start-up pitches on all continents, I decided to gather some of my thoughts based on this extremely rewarding professional journey at Mountain Partners. Reach out!

Some helpful sources I used:

https://mattermark.com/about-venture-capital-returns-valuations/

https://mattermark.com/irr-important-vc-performance-metric-thats-also-nearly-impossible-use/

📝 Read this story later in Journal.

🗞 Wake up every Sunday morning to the week’s most noteworthy Tech stories, opinions, and news waiting in your inbox: Get the noteworthy newsletter >